Since 2017, another form for compiling statistical reports of 7-NDFL has been used in the structures of the tax service of the Russian Federation. In 2020, the timing of its formation remains unchanged. For this form, data from the 6-personal income tax report provided by legal entities and individuals for the reporting period is used. Form 7-PIT displays the information received for each quarter, as well as a summary for the year.

Normative base

The new report 7-NDFL was put into operation by order of the Federal Tax Service of November 30, 2016. Order No. MMV-7-1 / 647 @ regulates the use of statistical tax reporting forms for 2017. In 2020, there were no changes regarding this reporting form, therefore, the provision of data should be performed as usual.

Report 7-NDFL is an internal document of the tax structure and is compiled by employees of the regional branches of the Federal Tax Service. In the future, data is collected on the subjects of the Russian Federation to compile a common consolidated form throughout the country.

In November 2017, the Federal Tax Service published a letter No. ГД-4-11 / 23247 @, on conducting quarterly monitoring of summary data on 7-NDFL. The letter was written to motivate employees of the Federal Tax Service of the Russian Federation to pay more attention to the quality and reliability of the information provided.

To do this, managers of regional UNFS must adhere to the following requirements:

- identify the employee responsible for the preparation of the 7-personal income tax report (his position should be no lower than the deputy head of the department);

- strictly adhere to the timing of the provision of information;

- check control ratios, which should be within the range of acceptable values;

- correct critical inconsistencies (if any) within one calendar month;

- in case of impossibility to correct the discrepancies, submit an explanatory letter to the Department of taxation of personal income of individuals within 10 days.

Download the full text of the letter No. GD-4-11 / 23247 @

Deadlines

Order No. MMV-7-1 / 647 @ in Appendix No. 18 contains guidelines for filling out Form 7-NDFL. In 2020, the authorized employees of regional UFNS should provide statistical information to the FKU “Tax-Service” of the Federal Tax Service of the Russian Federation in terms that depend on the reporting period:

- for the I quarter - tentatively until June 22, 2020;

- for the half year - tentatively until September 22, 2020;

- for 9 months - tentatively until December 22, 2020;

- for the whole of 2020 - tentatively until May 22, 2021.

Dates are indicated on the basis of data from order No. MMV-7-1 / 647 @ and are recommended for use in the absence of clarifying documents.

Explanation

In some cases, an authorized person of the tax authority may request clarifying information in case of mismatch of any indicators in the form of 7-personal income tax. This means that the accountant must verify the data in the 6-personal income tax report, which is usually reported in the information request.

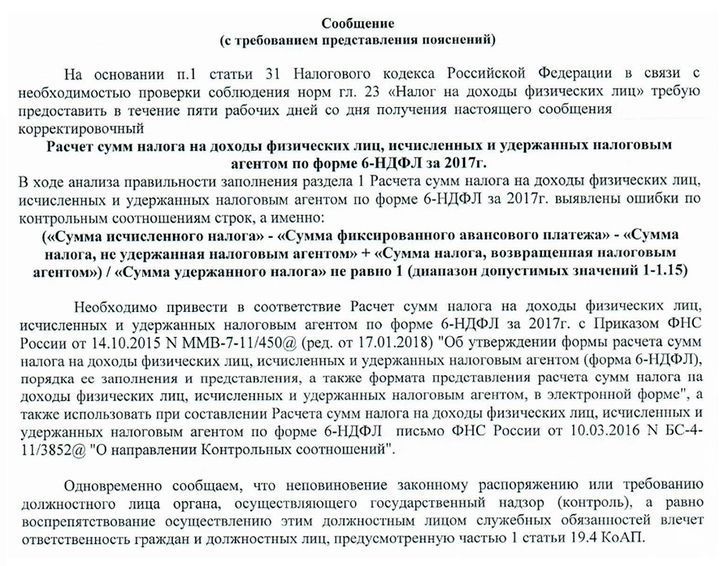

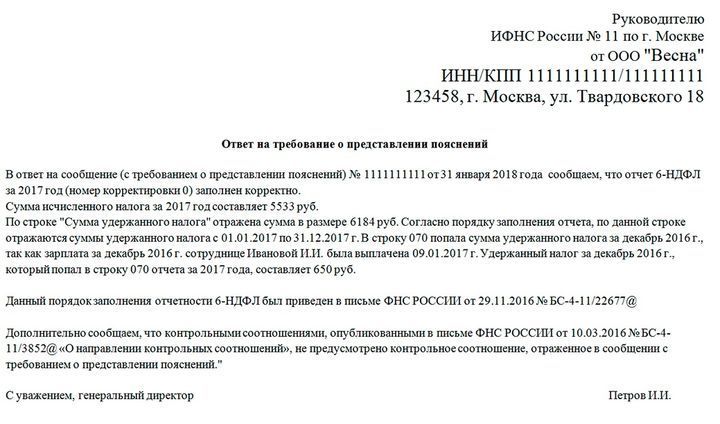

An example of a message from the tax inspectorate for explanations and an approximate response to it:

The correctness of reports is often checked against the control ratios established by the Federal Tax Service. If the data do not coincide with the specified range, the inspector may require clarifications or make appropriate adjustments. Such requests require a mandatory response, even if all reports are prepared correctly. In this case, it is necessary to indicate that no deviations were found and control ratios are satisfied.

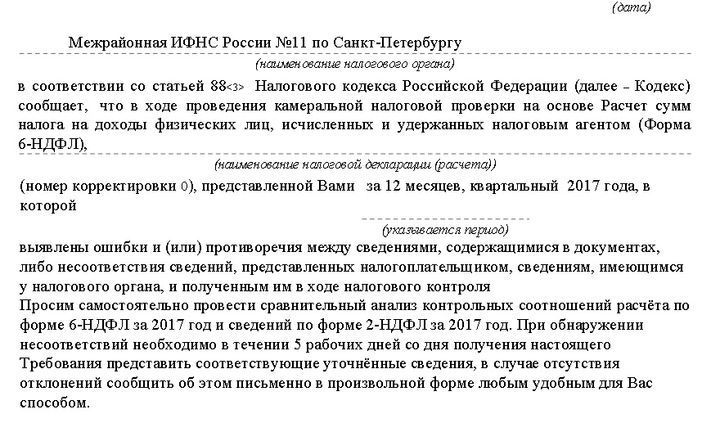

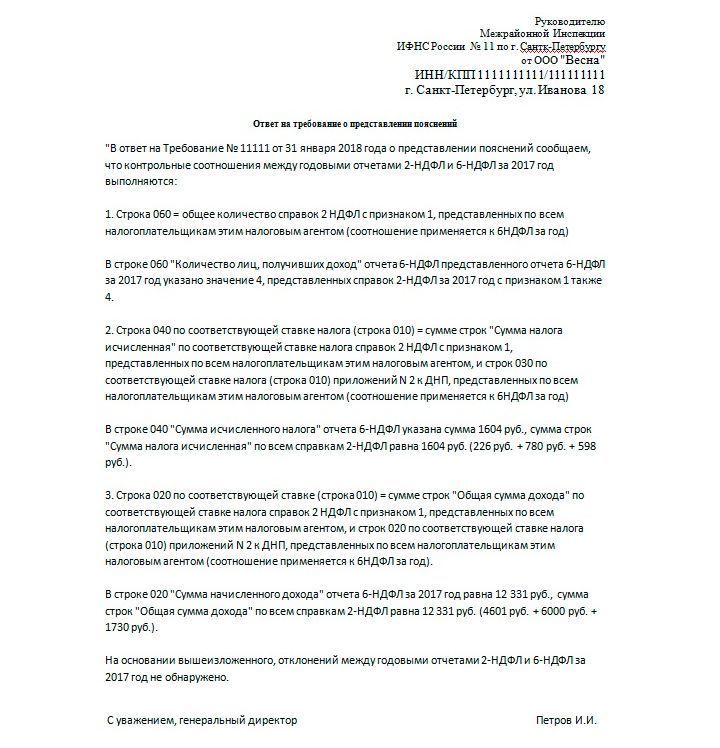

An example of a similar request and response to it:

All received messages from the IFTS must be answered. For this, 5 working days are provided, starting from the day after the date of receipt of the notification.

Filling 6-personal income tax

In order to eliminate inconsistencies in the preparation of the 7-NDFL report, the enterprise (both the legal entity and the individual entrepreneur) must provide the correctly completed 6-NDFL form. This report should be compiled by all companies that employ employees in their activities. Form 6-NDFL is essentially a generalization of 2-NDFL. The difference is that 2-personal income tax reflects the income and expenses of each employee, and 6-personal income tax - in general.

Form 6-NDFL is compiled every quarter, on an increasing scale, taking into account previous periods:

- for the I quarter (until April 30);

- for the half year (until July 31);

- for 9 months (until October 31);

- for the whole year (until April 1 of next year).

Detailed instructions for filling out 6-NDFL are formulated in the order of the Federal Tax Service of October 2015 No. MMV-7-11 / 450 @. You can see the full version of the document on the official portal of the Federal Tax Service www.nalog.ru/rn77/about_fts/docs/5797895/. The main requirements include the following points:

- data is filled from left to right, starting from the very first cell;

- blank cells must be marked with dashes;

- when dividing the form into two parts, the left one is filled in by an employee of the enterprise, and the right one is filled in by a tax inspector;

- forms are forbidden to print on both sides;

- When filling out the electronic version, the Courier New font is used in size 16-18.

The following information must be entered on the title page:

- TIN and KPP (for legal entities, IP put dashes);

- adjustment number (zeros are put for the original document, if corrections have already been made - 001, and so on, depending on the number of adjustments);

- code of the reporting period (for example, code 21 is assigned to code 21, for half a year - 31, etc. - the information is specified in order No. MMV-7-11 / 450 @) and year - 2020;

- tax inspection code where the document is filed;

- submission code (also indicated in the order);

- Name of individual entrepreneur or name of legal entity;

- OKTMO;

- phone number;

- number of pages in the document.

Sections 1 and 2 are filled on the second page of the form. If employee income for the specified period is taxed at different interest rates, then Section 1 must be filled out separately for each tax amount. At the same time, in the section “Results for all lines” summarizes information on all tax rates. This data is recorded only on the second page, dashes are placed on others.

The lines of the sections indicate which quantities are required for them. Section 1 describes general information and employee income, taxes paid, costs and deductions. If the employer does not have data for certain lines, then zeros are put in them, not dashes.

If the employer pays wages in the current month, then the value in line 040 should correspond to the number in 070. If some amount was not withheld, then it is displayed in line 080. In this case, 040 will be 070 + 080.

Section 2 describes employee income and withheld amounts by date. The charge date should be taken into account here. PIT will be withheld after the actual payment of money. And the receipt of funds in the budget occurs on the day after payments.

As a result of filling in the information in Section 2, the sum of all lines 130 should coincide with 020, and the total value of lines 140 should coincide with 070.

Read also:

- Application for personal income tax return in 2020

- 2 personal income tax in 2020: deadlines, form, changes

- The average number of employees in 2020

(No ratings yet)

(No ratings yet)